AE Wealth Management: Weekly Market Insights | 2/19/23 – 2/25/23

Weekly Market Commentary

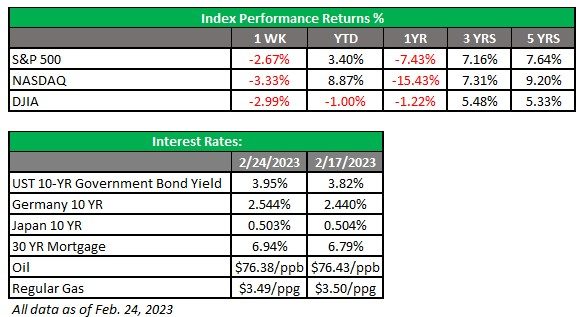

THE WEEK IN REVIEW: Feb. 19 – Feb. 25

Market grapples with higher rate expectations

Despite one less trading day last week, we managed to pack in a lot of activity. The markets had another rough week with angst over what the Federal Reserve will — or will not — do at its next few meetings. Last Tuesday was the worst day of the year so far, with the Dow shedding nearly 700 points and the S&P 500 dropping 2%.

Yields, which have marched upward since the beginning of February, continued to climb after hotter-than-expected economic data dispelled all hopes of a Fed pause anytime soon and the possibility of cuts in the back half of 2023. The 10-year U.S. Treasury note neared 4% in a sign of trouble for the equity market, while Home Depot and Walmart offered disappointing guidance. The two retailers signaled they were expecting a tough year for the retail industry and gearing up for a consumer slowdown.

Markets grappled with this information while also keeping a close eye on the release of the Fed minutes, which showed the Fed was nowhere close to considering a pause, let alone cuts. In fact, the minutes showed that some Fed members favored a 50-basis-point (.50%) hike over the increase of 25 basis points (.25%) we got at the last meeting.

The week ended on a sour note as the core personal consumption expenditures (PCE) index, the Fed’s preferred measure of inflation, reversed course in January. The reversal is a sign that the Fed may have to be more aggressive than expected and a worrying indicator for investors who are already nervous about stubbornly rising prices. Markets dropped off again on Friday, eroding the year’s strong gains as we near the end of February.

Given the current data, it’s highly improbable that the “rate easing in the second half of 2023” narrative the market has been hanging onto the past few months is worth any consideration. In fact, it may be completely out the window. It seems the best we may be able to expect is a pause in rate hikes, which is now considered the new version of a rate “cut” as far as the market is concerned. The biggest concern is that the data will deteriorate significantly faster, and the Fed will have to reverse course in response, making a severe recession inevitable. There is less and less talk of a potentially soft landing for the economy, and it appears the Fed could fly blindly past the airport on this one.

Q4 GDP revised downward

The second reading of fourth-quarter 2022 gross domestic product (GDP) was released last Thursday, moving downward from 2.9% to 2.7%. Sure, two-tenths of a percent may not seem like a big deal, but the reason given for the downward revision was. The main reason cited was a slowdown in consumer spending which, despite inflationary pressures, has been holding up. This may be the beginning of what we have previously said would occur if the consumer begins to lose confidence and reaches a point of consumption exhaustion. It’s a collective economic “shop ‘til you drop” with the “drop” part front and center.

The Fed has focused on mitigating wage inflation and inflation in general by trying to increase unemployment and slowing the economy by raising rates. So far, higher unemployment hasn’t materialized, the economy is still growing and inflation remains elevated. However, consumers are maxing out credit cards with higher rates, making the servicing of revolving debt more expensive, while real wages and buying power are declining. Prices remain elevated and the consumer is flagging.

The Fed keeps raising rates and has yet to see its efforts result in the desired outcomes of significantly lower inflation and a cooling job market. That’s why the consumer spending slowdown is concerning; until now, the consumer has been the counterbalance to the Fed’s aggressiveness. If the consumer pulls back or collapses, the combination of that and everything the Fed has done so far will have a harsher impact on the economy.

The perfect storm of higher rates and a spending collapse could tank the economy, and the Fed might have to turn immediately around and start lowering rates aggressively, creating a whipsaw effect. This is why we’ve been supportive of the idea of a Fed pause in early 2023: Let the current interest rate levels have their full impact instead of continuing to raise rates in response to past data, which may or may not be reflective of current reality. In any case, a weakened consumer is not a welcomed sight.

Coming This Week

- Pending home sales on Monday will provide the temperature of the real estate market.

- Chicago producer manufacturing index (PMI), Case-Shiller Home Price Index, consumer confidence and the Richmond Fed Manufacturing Index will all be released Tuesday.

- On Wednesday, we’ll see mortgage applications and the Survey of Business Uncertainty numbers.

- Car sales and the Fed balance sheet will be released Thursday.

- Finally, Thomas Barkin (Richmond Fed) and Raphael Bostic (Atlanta Fed) will close out the week with speeches on Friday.

- Although any one of the data points mentioned above may not move markets on their own, the sheer volume and complexion of the data may set a tone. If reports shade to the brighter side, the markets may perk up. But markets will likely stay edgy if the data trends to the negative.

AE Wealth Management, LLC (“AEWM”) is an SEC Registered Investment Adviser (RIA) located in Topeka, Kansas. Registration does not denote any level of skill or qualification. The advisory firm providing you this report is an independent financial services firm and is not an affiliate company of AE Wealth Management, LLC. AEWM works with a variety of independent advisors. Some of the advisors are Investment Adviser Representatives (IAR) who provide investment advisory services through AEWM. Some of the advisors are Registered Investment Advisers providing investment advisory services that incorporate some of the products available through AEWM.

Information regarding the RIA offering the investment advisory services can be found on https://brokercheck.finra.org/.

Investing involves risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values.

The information and opinions contained herein, provided by third parties, have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed by AE Wealth Management.

This information is not intended to be used as the sole basis for financial decisions, nor should it be construed as advice designed to meet the particular needs of an individual’s situation. None of the information contained herein shall constitute an offer to sell or solicit any offer to buy a security or insurance product.

2/23-2722061-4