AE Wealth Management: Weekly Market Insights | 2/20-2/26/22

VIEW PDF VERSION

Russia invades and markets shrug

The much-predicted and anticipated invasion of Ukraine finally kicked off last Thursday. Russian forces launched “security operations” after declaring two breakaway regions (Luhansk and Donetsk) in the Donbas “independent.” As soon as these regions were declared independent, they asked for help from Russia to protect them against Ukrainian “aggression” — which was all the pretext Russia needed to launch the invasion currently in progress.

The European Union, U.S. and NATO all condemned the hostilities; many speeches and proclamations were made while stiff sanctions were threatened and no mention was made for supporting the Ukrainian military. When initial sanctions were announced, they were pretty weak and far short of the type of debilitating sanctions we were led to believe would be imposed. If we expect weak sanctions to reverse the invasion, there really isn’t much hope for Ukraine. RIP Ukraine (1991-2022): 30 years of post-Soviet independence appears to be over.

Later in the weekend, more serious sanctions were announced to hurt Russia financially, including removing Russian banks from the global SWIFT payment system and cutting off the Russian Central bank. Sanctions, in general, really hurt the ordinary people and not the leadership of an offending country. In this case, the sanctions will do neither. The only meaningful — and perhaps most meaningful — sanction that would grab Russia’s attention has not been addressed: and preventing them from selling oil and gas around the world.

Once the U.S. markets caught wind that pretty much nothing coming out of the White House was going to upend global financial and energy markets, there was an . The Dow clawed its way out of a negative 850-point hole in the immediate aftermath of the invasion news. Meanwhile, the S&P 500 was down 2.5% at one point but ended the day up 1.5%. On Friday, the markets had their best day so far in 2022 as reports said President Vladimir Putin was prepared to discuss peace. How real are these offers of peace? That’s anyone’s guess. But given Putin’s propensity for saying one thing and doing another, we wouldn’t put a lot of stock in that news. For their part, markets were very eager to believe, and we barely dipped into correction territory before markets rebounded on Friday.

Then over the weekend, Putin announced a higher alert posture for his nuclear force, signaling an ominous potential for escalation as his hopes of swiftly toppling the Ukrainian government has not occurred and Ukrainians appear to be mounting a stiff resistance. That news slapped markets in the face first thing Monday morning.

The repercussions of how we handled this situation and Afghanistan before it shows that geopolitical risk is a potential market disrupter. Putin flexing his nuclear muscles should serve as a reminder of why Iran should not be allowed to develop nuclear weapons capabilities. Next on the horizon is whether Putin continues to behave aggressively toward his neighbors or whether China begins to act out toward Taiwan. This situation will continue to weigh on the markets in the next few weeks as we move right up to the next major event: the Federal Reserve meeting in March and how it will deal with inflation.

The Fed’s treacherous path

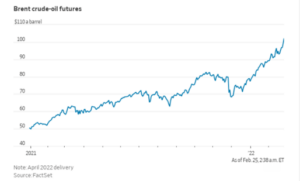

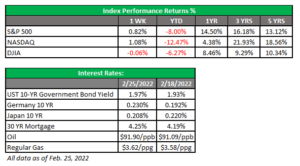

Last week, we laid out how we got to 7.5% inflation and how both the Fed and the federal government were complicit in the situation. Both bodies made missteps along the way, and we have yet to find a more durable solution to the insidious rise of inflation. The current Ukraine situation has provided some cover to the administration. They will claim that the most recent spike in prices or supply chain issues was Russia’s fault, even though there has been no sanctioning of oil exports from Russia and we import very little from them. Oil continues to hover near $100 per barrel, levels we haven’t seen since 2014. The price of oil has climbed steadily since late 2020, and the average price for regular unleaded in the U.S is $3.62 per gallon, pretty much what it was before the invasion.

President Joe Biden has stated that he viewed the Fed as the appropriate institution to slow and tame inflation. After last week’s invasion, the chance of a 50 bps (.50%) interest rate hike at the March meeting has decreased to 13%. If the Fed remains dovish (or reluctant to raise rates) in the face of inflation, who do they have to blame? We discussed the policy mistakes the Fed has made last week, and it appears they aren’t over their first mistake, which was believing that inflation was “transitory.” It also seems that the Fed believes going slowly and timidly will be enough and inflation will just fade away on its own.

This upcoming Fed meeting is crucial, yet it may result in a missed opportunity and put us behind even further in the fight against inflation. This will only result in having to take even more drastic measures later as things get worse. When we finally come to grips with what needs to be done to fix inflation, it may be too late, as we may already be well on our way to a recession and a lot of pain in the stock market.

Coming This Week

- We’ll have plenty of data this week as we continue to deal with the fallout of the Ukraine situation.

- Retail and wholesale inventories will be announced on Monday, while construction spending and motor vehicle sales will be released on Tuesday and Wednesday, respectively.

- President Biden will deliver the State of the Union address on Tuesday.

- By midweek, we’ll start to get an idea of the jobs picture for February. ADP will release its employment report on Wednesday, weekly unemployment claims will be reported on Thursday and the Bureau of Labor Statistics (BLS) non-farm payroll report for February will come out on Friday. Last month, the BLS reported the creation of 467,000 jobs.

- We’ll also have Fed speakers all week. This is important because it can yield insight into what Fed officials are thinking in advance of their March meeting.

- Remember, anything can happen in Ukraine — and those events could impact markets. Keep in mind that the very real possibility of cyberattacks on the U.S. by Russia is still alive.

Have a great week!

Tom Siomades, CFA®

Chief Investment Officer

AE Wealth Management

AE Wealth Management, LLC (“AEWM”) is an SEC Registered Investment Adviser (RIA) located in Topeka, Kansas. Registration does not denote any level of skill or qualification. The advisory firm providing you this report is an independent financial services firm and is not an affiliate company of AE Wealth Management, LLC. AEWM works with a variety of independent advisors. Some of the advisors are Investment Adviser Representatives (IAR) who provide investment advisory services through AEWM. Some of the advisors are Registered Investment Advisers providing investment advisory services that incorporate some of the products available through AEWM.

Information regarding the RIA offering the investment advisory services can be found on https://brokercheck.finra.org/

Investing involves risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values.

The personal opinions expressed by Tom are his alone and may not be those of AE Wealth Management or the firm providing this report to you. The information and opinions contained herein, provided by third parties, have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed by AE Wealth Management.

This information is not intended to be used as the sole basis for financial decisions, nor should it be construed as advice designed to meet the particular needs of an individual’s situation. None of the information contained herein shall constitute an offer to sell or solicit any offer to buy a security or insurance product.