AE Wealth Management: Weekly Blog Insights | 3/13-3/19/22

VIEW PDF VERSION

Ukraine situation grows grimmer, oil rise stalls and the markets breathe a sigh of relief

More horrific images came out of Ukraine this week, as Ukrainian President Volodymyr Zelenskyy made an impassioned appeal to the U.S. Congress for more aid in his country’s fight against Russia. As we enter the fourth week of the conflict, it appears the Russians have stalled and are resorting to increasingly brutal measures to subdue the Ukrainians. Digging tanks into defensive positions and bombing civilians doesn’t seem like some sort of grand strategy, but then again, who knows what’s in Putin’s mind?

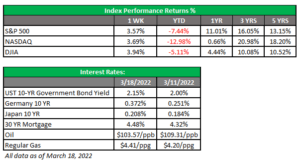

While “talks” between the Russians and Ukrainians stalled last week, the price of oil dropped below $100 per barrel briefly and the Federal Reserve delivered its much-telegraphed 25 basis point (.25%) rate hike. Plus, President Joe Biden spoke with Chinese leader Xi Jinping. That was all the markets needed to stage a relief rally of about 1,500 points on the Dow to end its miserable five-week losing streak.

Was the approximately 5% rally the beginning of something? It appears unlikely. We still have unresolved issues, including the Ukraine-Russia war, ongoing inflation (more below) and the global oil supply issue (and tangentially energy and gas prices). Basically, we’re no better off than we were two weeks ago, apart from the Fed finally doing what we all knew it would do. Therefore, it doesn’t seem like this is the start of a prolonged rally that could erase this year’s losses so far.

Some good news: Volatility has come down from 33 at the beginning of last week to 25 by the end of the week. Oil also came down below $100 per barrel last week, giving the markets a chance to breathe. Volatility is still elevated by historical measures, and $100 per barrel isn’t good — but relatively speaking, volatility of 25 is better than 33 and $100 is better than $130 for a barrel of oil.

We still need to be careful, however. Anything can happen in Ukraine, and we still do not have a clear indication of where China ends up in all this. We also don’t know what we’re prepared to do if China doubles down in its support for Russia and defies the West and its sanctions — or what Russia might do if it feels China has abandoned them. The ripple effect on our economy would be immense, so geopolitics remain front and center. Closer to home, we’re still grappling with our own internal struggles of inflation, high gas prices and supply chain issues. It’s hard to understand why the markets are as buoyant as they are given the current backdrop.

The Fed makes its move!

The 25 basis points (.25%) rate increase last week was a given. The surprise? There will be six more hikes this year. The move was largely telegraphed, so it was priced into the markets. Markets dipped immediately after the announcement, but once they figured out that the Fed was once more making equities what may be the only real option for investors, they took off again.

When the U.S. 10-year Treasury was trading below 2% and inflation was running at 2% to 3% per year, we were looking at a flat or slightly negative real return. People piled into stocks and went yield hunting in some sketchy places. Now the 10-year is over 2% but inflation is at 7.9% and rising. Where will people turn when the net negative real return is closer to 6% versus being flat before? And if the 10-year approaches 3% or 4%, they’ll still be upside-down by 4% even if inflation stops rising.

If stocks were the only game in town before, stocks will most likely be the place to be until the Fed gets serious. At least they stopped putting liquidity into the system and ended quantitative easing. A fed funds rate of 2% by the end of the year is not going to slow 8% inflation. The Fed has once more rolled over in accommodation to the stock market and has reinforced the concept of TINA (There Is No Alternative). They have also added to the likelihood of the economy slowing significantly or even moving into recession by year’s end or in early 2023.

Coming This Week

- After the Fed raised rates for the first time in three years, Fed officials will be on the road explaining why they did what they did and why it was the right move for the current environment. It will be interesting to hear what St. Louis Fed President James Bullard has to say, since he was the only voting member to dissent and proposed a 50 basis points (.50%) hike. Sadly, he is not scheduled to give any speeches.

- Thirty-year mortgages have risen to over 4% for the first time since May 2019. On Wednesday, we will see data for mortgage applications and new home sales. This might end up being the high-water mark for real estate if rates continue to rise for some time.

- Finally, on Friday we’ll see if consumer sentiment is showing any signs of improvement.

Have a great week!

Tom Siomades, CFA®

Chief Investment Officer

AE Wealth Management

AE Wealth Management, LLC (“AEWM”) is an SEC Registered Investment Adviser (RIA) located in Topeka, Kansas. Registration does not denote any level of skill or qualification. The advisory firm providing you this report is an independent financial services firm and is not an affiliate company of AE Wealth Management, LLC. AEWM works with a variety of independent advisors. Some of the advisors are Investment Adviser Representatives (IAR) who provide investment advisory services through AEWM. Some of the advisors are Registered Investment Advisers providing investment advisory services that incorporate some of the products available through AEWM.

Information regarding the RIA offering the investment advisory services can be found on https://brokercheck.finra.org/.

Investing involves risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values.

The personal opinions expressed by Tom Siomades are his alone and may not be those of AE Wealth Management or the firm providing this report to you. The information and opinions contained herein, provided by third parties, have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed by AE Wealth Management.

This information is not intended to be used as the sole basis for financial decisions, nor should it be construed as advice designed to meet the particular needs of an individual’s situation. None of the information contained herein shall constitute an offer to sell or solicit any offer to buy a security or insurance product.

03/22-2066555-3