AE Wealth Management: Weekly Market Insights | 5/15/22 – 5/21/22

View PDF Version

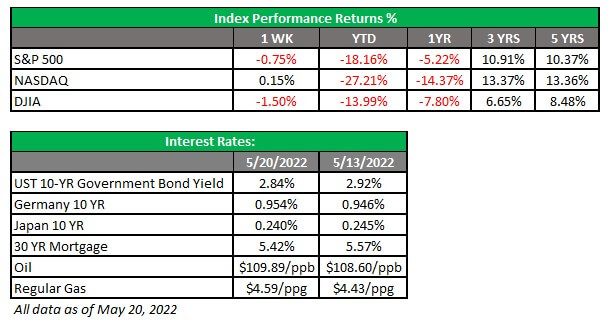

Markets drop for the 8th consecutive week

Entering the lair o’ the bear

Although earnings season is ending, there were some pretty prominent firms reporting last week that concerned the markets. Home Depot posted some solid earnings, leading to the only decent day last week. But the Home Depot report was bookended by dismal news from Walmart and Target. These two bellwethers of consumer spending are beginning to paint a dark picture of the consumer, which to this point has been the only real bright spot for the market to latch on to.

Inflation has been taking its toll on consumers; as pandemic stimulus and savings peter out and more income is diverted to higher gas, food and housing costs, people are beginning to pare down their discretionary spending. The negative gross domestic product (GDP) print from the first quarter already was signaling a slowing economy, and talk of recession has begun to dominate discussions. The Federal Reserve has also continued to talk tough, and unlike in the past when a jittery market was all the Fed needed to suspend plans to raise rates, Chairman Jerome Powell has not signaled the Fed plans to let up in its efforts to tame inflation and stop raising rates.

A slowing economy, weak consumer spending, cooling housing markets and high levels of inflation are all conspiring to send markets lower. There really is no place to hide other than commodities, which are the only bright spot right now. As we ended last week, the S&P 500 was on the verge of joining the Nasdaq in bear country (20% off the most recent highs). The eight-week slide in stocks is the longest consecutive streak in 90 years. It’s hard to point to a bottom, but more often than not, the bottom comes and goes before it’s apparent to anyone what is happening. If you have made it this far and your goals are still intact, don’t let media hysteria and hype make your paper losses into real losses. Don’t engage in wealth destruction and miss out on the rebound, which — although hard to predict — will eventually come about.

The Fed stays the course (for now)

So far this century, markets have always counted on the “Fed put,” the idea that the Fed will step in and provide accommodation if markets get beaten up too badly. The market has banked on this since the financial crisis, after the Fed stepped in (or stepped back) in 2008-2009, then again in 2013, 2018 and 2020. You really can’t blame the market for expecting the same this time around.

The problem today is that in those prior instances, we didn’t have an 8.3% inflation rate, so it was an easy decision for the Fed to come to the market’s rescue. Now a newly reappointed Fed Chair Powell feels it his duty to channel his inner Paul Volcker and solely focus on taming inflation. The story will get more interesting if we enter a recession, which will result in the unemployment rate increasing. Then the Fed will have to make the decision as to which of its two mandates it will focus on: price stability or job growth. Given the Fed’s tools, it cannot work both sides of the problem. It can either fix inflation (which will slow the economy and jobs will be lost) or it can be accommodative once more (which will spur growth and more jobs while inflation persists). It’s not a pleasant place to be, but here we are.

Coming This Week

- On Wednesday, the minutes from the Fed’s last meeting will be released. We’ve already seen where Chairman Powell stands, but the minutes may give us a glimpse of just how hawkish the other Fed members are.

- The second reading of first-quarter GDP is out on Thursday. It will be interesting to see if there is a meaningful revision of the initial -1.4% reading.

- Although earnings are almost done, some retailers and home builds will report this week, potentially adding fuel to recessionary concerns after Walmart and Target blew up last week. Watch for signs of slowing in new home sales on Tuesday and mortgage applications on Wednesday. With conventional rates hovering around 4% for a 30-year fixed-rate mortgage, we will likely see continued declines in the housing market.

- Finally, on Friday consumer confidence and spending will provide insight into just how bad things are for the consumer.

AE Wealth Management, LLC (“AEWM”) is an SEC Registered Investment Adviser (RIA) located in Topeka, Kansas. Registration does not denote any level of skill or qualification. The advisory firm providing you this report is an independent financial services firm and is not an affiliate company of AE Wealth Management, LLC. AEWM works with a variety of independent advisors. Some of the advisors are Investment Adviser Representatives (IAR) who provide investment advisory services through AEWM. Some of the advisors are Registered Investment Advisers providing investment advisory services that incorporate some of the products available through AEWM.

Information regarding the RIA offering the investment advisory services can be found on https://brokercheck.finra.org/

Investing involves risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values.

The information and opinions contained herein, provided by third parties, have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed by AE Wealth Management.

This information is not intended to be used as the sole basis for financial decisions, nor should it be construed as advice designed to meet the particular needs of an individual’s situation. None of the information contained herein shall constitute an offer to sell or solicit any offer to buy a security or insurance product.

5/22-2180545-4